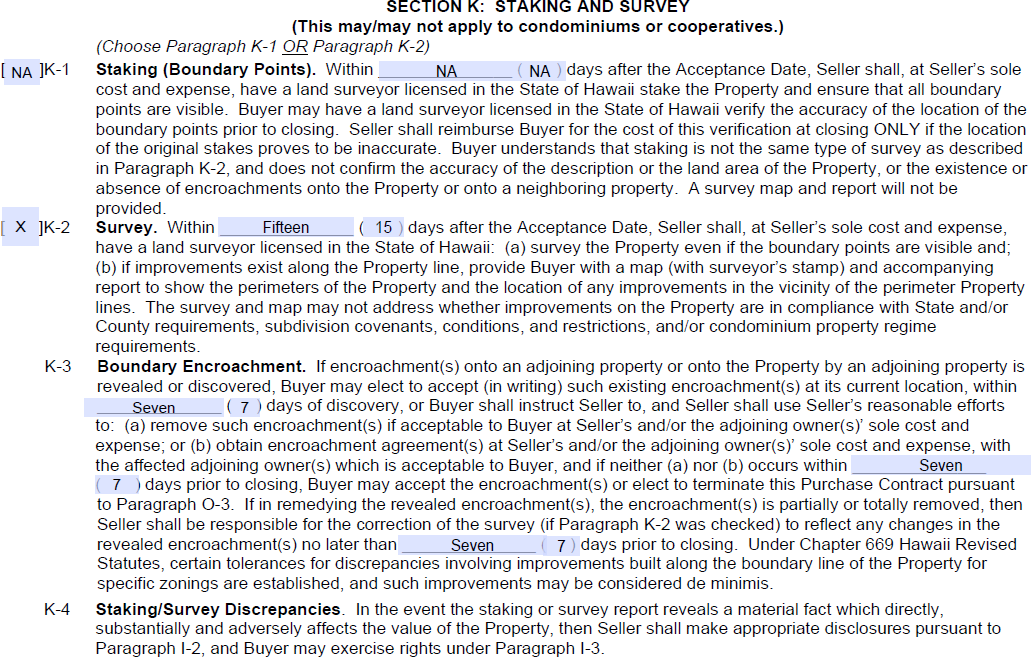

We always check K-2 for our buyers. It is a complete survey. K-1 is normally NA. For condos surveys are not possible. If the home is a CPR sometimes surveys are possible and sometimes they are not possible.

K-3 Boundary Encroachments

If a property has encroachments most of the time to buyer will continue anyway.

Most encroachments have been in place for years without an issue, so the new buyer will accept them.

Sometimes they want the seller to try and get an encroachment agreement and if so the attorney at escrow can draft one.

Encroachment agreements are not automatic, the neighbor must sign it, and many times they are not willing to do so.

The buyer can terminate the Purchase Contract if they are not comfortable with the encroachments and the seller is not able to get an encroachment agreement signed by a neighbor.

Paragraph J-8 shown below dictates when your stuff needs to be out, but it specifically says you can stay there until closing, although with all your stuff out of the house it is more like camping in your own home should you decide to stay until closing.

Some agents will say 5 days for J-8 as they want to conduct the final walk through with everything out of the property.

Before sellers plan to move out they should have their agent confirm the closing date. If the buyer decides they need an extension to close, there is no sense moving out 5 days prior to closing. For example, most extensions are 10 to 15 days and the buyer can automatically choose to extend. If there is a 15-day extension, and the seller moved out 5 days prior to closing, now the seller is out 20 days prior to closing. As there is no guarantee the buyer will close, moving out too far ahead of time could be an issue if the buyer ends up not closing.

Each seller has to make the decision on when to move out based on the contract and based on their personal situation in terms of where they are moving to.

Unfortunately there is a risk for sellers if they do fall out of escrow they could end up paying rent at their new place plus their mortgage payment, or 2 mortgage payments if they bought a new home. To prevent the two mortgage payments situation many sellers make the purchase of their new home contingent on selling their current home. This way if the home they are selling falls out of escrow, they are not obligated to buy the new home.

Additional Search Terms: Removal of Items from Property, J-8, J8, trash, junk, personal belongings

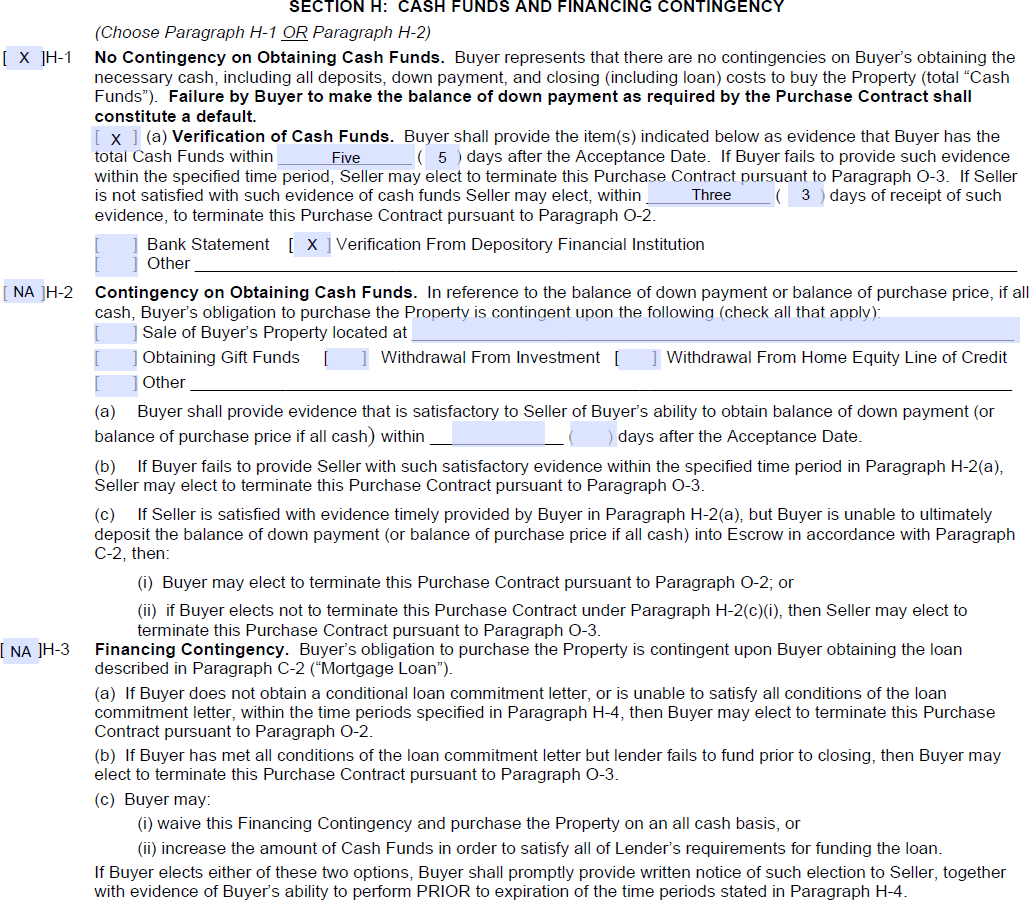

Escrow is most likely to fall out during the inspection period, but that happens early on in the escrow, normally within the first 2 weeks. After the inspection is approved and you are getting close to closing the most common reason escrow is cancelled is using the financing contingency.

Simply put, if the buyer can’t get their loan there is no way they can close. As long as they have not breached the contract prior, they can cancel and get all their deposits back.

This type of cancellation is the most frustrating for the seller, because the seller might have already moved out, rented or purchased another place, or maybe has a place in escrow and is counting on the funds from the home they are selling.

As bad as it is, there is really nothing that can be done when the lender says they can’t fund. You could look for another lender, but most likely the same reason the current lender can’t fund will come up and be an issue with another lender too.

One would wonder how the buyer got pre-approved only to find out they now can’t get the loan. Various factors can contribute to this, such as job loss, change of jobs, surprise on the tax returns, surprise liabilities, low appraisal, etc.

So what can a seller do to prevent falling out of escrow at the last minute from the finance contingency?

Typically the more money a buyer is putting down the less likely they are to fall out. Also you want to make sure you have a pre-approval, hopefully from a local lender, and you want to make sure they meet all the finance contingencies on time.

The biggest contingency is the conditional loan commitment letter. If this is late it could be a sign that the lender is having trouble committing to the loan and the reason it is late should be looked at closely.

We use 12 days before closing for the buyer to get the conditional loan commitment letter.

Getting a conditional loan commitment letter on time is one thing that is out of the buyer’s hands and relies on the lender.

Keep in mind if the lender is going to be late an extension must be requested, otherwise the buyer has breached the contract and the seller may elect to terminate the Purchase Contract.

If the buyer misses any of their loan deadlines the seller can cancel. However, normally it makes more sense for the seller to inquire as to why the deadline was missed and provide the buyer extra days if needed to prevent having to start again with a new buyer.

Low Appraisals – If the appraisal is low the first thing to do is to get a copy of it to look at the comparables used. Getting an appraisal changed is very difficult. If you have a strong issue with one of the chosen comps you can bring it up with the buyer’s agent and the buyer’s lender. Appraisers will have very good arguments on why they did what they did. Their job depends on doing it right, so they will be prepared to back up the appraisal. Having a bad appraisal is like saying they do not know how to do their job. That is why it is so difficult to get one changed.

If the appraisal is not changed the buyer will most likely request to pay the appraised price. Sellers can either accept this request, negotiate, perhaps to something mid-way between the appraised price and the Purchase Contract price, or stick with the price on the Purchase Contract.

If the buyer can’t get the loan at the Purchase Contract price because of the low appraisal, then they would have the right to cancel. If they can still get the loan even though the appraisal is low, then they do not have the right to cancel using H-3.

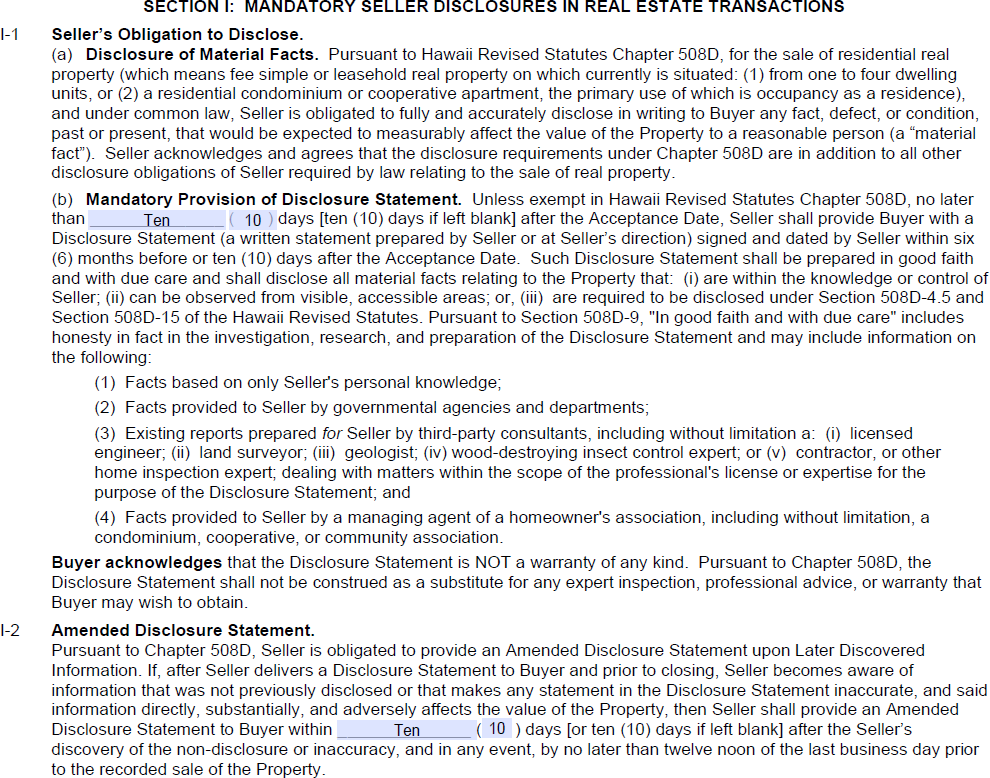

A complete disclosure is the most important thing a seller can do to protect themselves from being sued in the future.

The rule I go by for the disclosure is if you must think about whether an issue is important enough to disclose, then you should disclose it.

The rule our attorney gives us is you won’t get sued for something you disclosed, it is only when you don’t disclose something that you could get sued.

Almost all lawsuits from unhappy buyers have to do with something that was not disclosed.

There is a comprehensive disclosure statement with many questions that sellers will answer and provide to the buyers, normally within 10 days after acceptance.

If a new disclosure comes up, or one that makes a previous disclosure statement not accurate, and this disclosure substantially affects the value of the property, then the seller needs to provide an Amended Disclosure Statement to the buyer. Substantially is a keyword as minor issues that can easily be fixed do not create the need for an Amended Disclosure Statement.

If the buyer is not satisfied with the disclosure statement or amended disclosure statement, they have up to the number of days in I-3 to cancel the escrow and get their deposits back.

The “As Is” Conditional Addendum does not change the seller’s responsibility to disclose everything.

So sellers make sure you disclose everything. This is the most important thing you can do to make sure you are not sued after the sale closes.

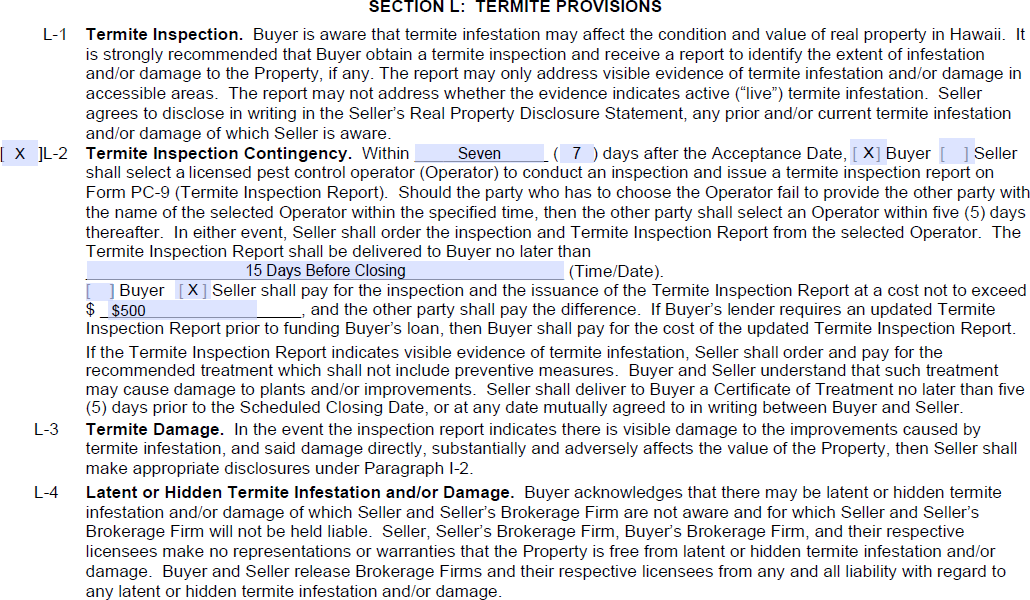

Sellers should have the buyer to select the termite inspector. This is for the seller’s protection. If the seller selects the inspector and there is a mistake now it is the seller’s problem. If the buyer chooses the inspector and there is something missed it is the buyer’s issue.

Normally the inspection is done 15 days before closing. Some lenders won’t allow it to be older than 30 days and there is no need to do it right away in case the buyer cancels you don’t want to pay for it and then have the buyer cancel as you will need a new one for the next buyer.

We can order the termite inspection when the time comes, and it can be billed through escrow.

The seller almost always pays for the termite inspection. Some put actual cost which is OK because we have never seen a termite inspector charge too much.

If there are live termites then you will need to pay for the treatment, which is tenting unless tenting is not possible. If tenting is not possible spot treatment would be recommended.

Seller’s select the company to do the termite treatment.

Per paragraph L-3 if substantial termite damage is found than it has to be disclosed. This new disclosure then gives the buyer a chance to cancel if they are not comfortable with the damage found. If the damage is minimal and does not affect the property value then the buyer can’t cancel.

Critical paragraph from the As Is Addendum showing it does not change the contract and full disclosure is still needed

The “As Is” Conditional Addendum sounds intimidating, but if you look at it closer, it does not mean much.

It does not change any of your rights during the inspection. You can still cancel, ask for credit, or ask for repairs.

It does not change the seller’s responsibility to disclose everything on their disclosure statement.

It specifically says that the Purchase Contract overrides the “As Is” Conditional Addendum, so if you call for something to be repaired in the contract, this overrides the “As Is” Conditional Addendum.

It does not even help the seller after closing because it specifically says they are still liable for claims where they did not disclose a material fact. So the buyer can still sue after closing. As almost all lawsuits are because of an undisclosed material fact, the As Is specifically says the seller is still liable in these situations.

So, what does it do for the seller then? It simply sends a message that they prefer not to do repairs. Buyers can still ask for repairs, but sellers are saying up front that they prefer not to do any.

We feel one of the most important things we can do for a buyer or seller is to help them close. Along these lines we do not sweat the small stuff on Purchase Contracts.

I see some agents change 3 days to 5 days, 12 days to 10 days, and they keep making the tiny changes that really mean almost nothing. I am not sure if they just want their client to feel like they are doing something, or they really believe those changes are needed.

We feel changing the inspection from 12 days to 10 days is not important. The goal is not to get the longest inspection period possible, the goal is to close on the home. If you focus on the goal, you can see those small changes are not needed. Plus, once in escrow if you feel an additional inspection is needed, you can always request a small extension, and we pretty much always see sellers grant this small extension as they do not want to fall out of escrow.

Attorneys are notorious for making a ton of changes. I can always tell if the Realtor is also an attorney by the number of changes to the contract they make. Attorneys work with contracts all the time, and they feel their job is to make it as beneficial as possible for their client, so even though they are also a Realtor they still wear their attorney hat and make a ton of changes. Unfortunately, attorneys forget that as a Realtor their goal is to get the client into a new home, not just get them into a favorable contract. I have seen attorneys that make so many changes to the contract, the seller says no thanks, so they actually lost their client’s dream home because of their need to make so many changes to the contract.

So our advice is don’t sweat the small stuff. Focus on the big things like price and how long until closing and if the other terms are within a reasonable range don’t counter them. Focus on getting the home!

If you are lucky enough to get a counter offer in a multiple offer situation, you really want to accept it unless there is something major that you can’t live with.

You have to keep in mind a counter offer can be withdrawn at anytime. It might have a response required within 24 to 48 hours, but at anytime and without warning the seller can withdraw that counter offer and accept another offer. Once both parties have signed the counter offer, then it is binding and you are in escrow, but until that time the seller can withdraw as desired.

So if you are OK with the price but there are some minor things you would like to change we suggest not changing them and just living with those minor things.

Sometimes small things can be negotiated during the escrow process. For example, say you wanted a 15 day inspection period, but they countered with a 10 day inspection period. Well 8 to 9 days into the inspection if you still need more time you can let the seller know. We have found that sellers do not want to fall out of escrow, so while they were reluctant to allow 15 days prior to going into escrow, they would probably OK a 5 day extension rather than falling out of escrow and having to start again. Falling out of escrow has a stigma about it, buyers will wonder what went wrong, so sellers prefer to stay in escrow and close if at all possible.

So keep this in mind if you are in a multiple offer situation and receive a counter offer. If possible sign it right away, get into escrow, and if a few minor details need to be discussed once in escrow that is OK.

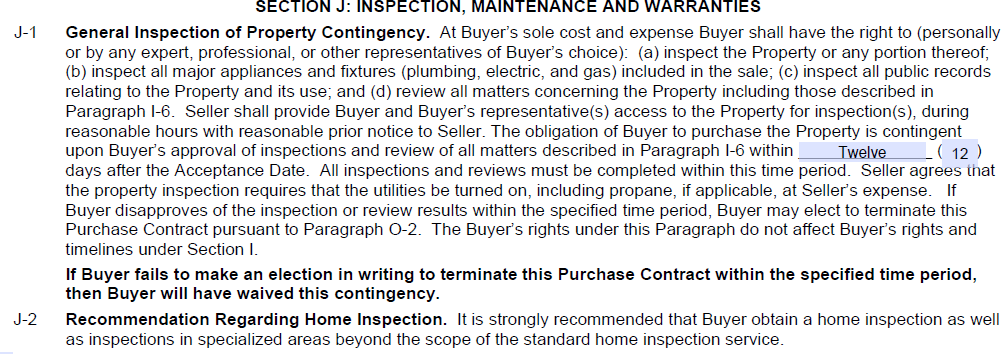

This is the buyer’s opportunity to inspect everything about the property. We recommend using a professional home inspector. Sometimes additional inspections are needed by plumbers, electricians, roofers, etc.

At any time during this period and for any reason the buyer has the right to cancel and get all their deposits back.

After the inspections are completed, but prior to this contingency expiring, the buyer may ask to have repairs done or a credit. A credit is normally an easier solution for the seller and therefore more likely to get approved.

The seller is under no obligation to do any repairs nor give any credit, so it is a negotiating process.

If an agreement is not reached the buyer has the option to cancel and get their deposits back or continue.

Keep in mind the As Is agreement has no impact over this contingency and buyers can still do everything mentioned above even if the As Is was used.

The normal time for this contingency is 7 to 15 days. If it is over 15 days, it will normally be countered.

It is important to understand that if the buyer does not make an election to cancel the Purchase Contract prior to this contingency expiring, then they have waived this contingency. This means even if negotiations are still going on for a repair or credit past the expiration date, then by default the buyer has waived their right to cancel using this contingency.