The numbers don’t lie — and they paint a sobering picture for anyone who invested in Chinese real estate over the past two decades.

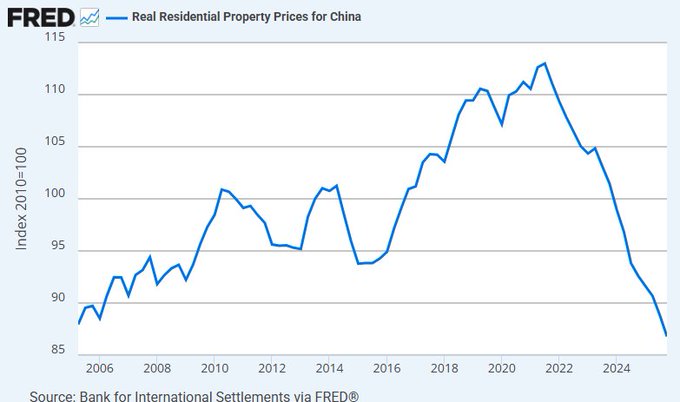

According to the Bank for International Settlements data tracked by FRED (Federal Reserve Economic Data), China’s real residential property prices (inflation-adjusted, indexed to 2010=100) have collapsed back below their mid-2000s levels. As of Q1 2026, the index sits at approximately 85.1 — lower than readings from 2006. After peaking above 112 in 2021, the market has given up all its gains and then some.

Anyone who bought a home in China since around 2006 is now underwater in real terms. That’s a staggering reversal for what was once seen as one of the most reliable wealth-creation machines in the world.

The Epic Boom (2000s–Early 2020s)

China’s property market was the engine of its economic miracle. Rapid urbanization, a growing middle class, easy credit, and massive government infrastructure spending fueled explosive demand. Real prices roughly doubled from the mid-2000s to their 2021 peak. In many cities, apartments became the primary savings vehicle for families — often viewed as safer than stocks or other investments.

For years, it felt like a one-way bet. Prices kept climbing through global financial crises, pandemics, and policy tweaks. Developers like Evergrande built empires on ever-increasing debt, pre-selling unfinished homes to eager buyers. Property and related sectors accounted for a massive chunk of China’s GDP — estimates often ranged from 25–30% when including construction, steel, appliances, and finance.

The Turning Point and Brutal Bust

The party started winding down around 2021. Years of warnings about excessive leverage culminated in strict government policies, most notably the “three red lines” debt caps on developers. Beijing’s messaging shifted dramatically under Xi Jinping: “Houses are for living in, not for speculation.”

What followed was a classic credit crunch:

- Major developers defaulted or restructured massive debts.

- New construction and sales plummeted.

- Buyer confidence evaporated amid unfinished projects, falling prices, and economic uncertainty.

- Local governments, heavily reliant on land sales, faced revenue shortfalls.

The result? A multi-year downturn that has seen real prices decline steadily since the 2021 peak. Year-over-year declines in new and second-hand home prices have persisted into 2025 and 2026, with some cities reporting drops of 5–8% or more in recent quarters.

Where Things Stand in 2026

The latest data shows no immediate bottom. Real prices continue trending lower, now trading below levels from nearly 20 years ago. High inventory, cautious buyers, and structural challenges (slower population growth, high youth unemployment, and shifting wealth preferences) are weighing on the market.

While the central government has rolled out various stimulus measures — interest rate cuts, easing purchase restrictions, and support for developers — recovery has been slow and uneven. Many analysts expect a prolonged period of adjustment rather than a sharp rebound.

Broader Implications

This isn’t just a housing story. The property slump has ripple effects across China’s economy:

- Household wealth: For millions of families, a huge portion of their net worth has evaporated.

- Construction and related industries: Massive job and activity losses.

- Local government finances: Reduced land sale revenues complicate debt servicing.

- Global knock-on effects: Lower demand for commodities like steel, copper, and lumber.

Yet China’s overall GDP has held up around 5% growth, driven by exports, manufacturing, and technology sectors. It’s a reminder that while property was dominant, the economy is rebalancing — albeit painfully.

Lessons for Real Estate Investors Everywhere

China’s experience is a dramatic case study in what happens when speculation, leverage, and policy risk collide. Key takeaways:

- No market goes up forever. Even seemingly unstoppable booms can reverse.

- Policy matters enormously. Governments can (and will) intervene when they perceive systemic risk.

- Transparency and data are critical. Independent, reliable price indices like the BIS series help reveal truths that official local statistics sometimes obscure.

- Diversification and risk management aren’t optional — they’re essential.

For those of us in markets like Hawaii, where real estate remains a core wealth-building tool, China’s story underscores the importance of sustainable growth, responsible lending, and avoiding bubbles. It’s also a reminder that while prices can fall sharply, well-located, high-quality properties in strong economies tend to recover over the long term.

The human cost — families who bought at the peak now facing losses — is the most painful part. Markets are cyclical, but the scars from this one will linger for years.